Gold Overtakes Treasuries in Global Reserves

Disclaimer: This article is for educational and informational purposes only and does not constitute financial advice, investment recommendations, or a recommendation to buy, sell, or hold any asset, including gold. All statements reflect publicly available data and general market analysis. Readers should consult a qualified financial professional before making any investment decisions.

By Doug Young – 05 June 2026

Introduction

Key Takeaway

Gold has surpassed U.S. Treasuries as the largest category in global central bank reserves, marking a significant shift in how nations allocate their monetary assets.

Why This Matters

The composition of central bank reserves influences currency stability, international payment capacity, and broader financial system resilience.

Changes in reserve allocation reflect evolving geopolitical dynamics and long-term strategic thinking among the world’s monetary authorities.

This article explains these developments in an educational manner and does not provide investment advice.

What Readers Will Learn

Readers will gain a clear understanding of recent reserve data, central bank gold purchasing patterns, the motivations behind sovereign gold accumulation, and what these trends mean for the global financial system.

Understanding Central Bank Reserves

What Are Reserve Assets?

Reserve assets are liquid foreign assets held by central banks and monetary authorities. They typically include foreign currencies, U.S. Treasuries, gold, and other instruments that can be used quickly to support the national currency, manage foreign exchange rates, and settle international obligations.

Traditional Reserve Composition

For decades, U.S. dollar-denominated assets, particularly U.S. Treasury securities, dominated global reserve portfolios. The dollar’s status as the world’s primary reserve currency made Treasuries the default choice for central banks seeking safety, liquidity, and deep markets.

Gold has historically served as a defensive asset, valued for its lack of counterparty risk and its role as a Store of value across centuries.

How Reserve Shares Are Calculated

Reserve shares are calculated based on the total market value of each asset category. This means that changes in asset prices can shift the percentage share even without new purchases or sales.

For gold, price appreciation can significantly increase its share of total reserves, while price declines can reduce it, independent of changes in physical holdings.

The New Reserve Data

Gold’s Share of Global Reserves

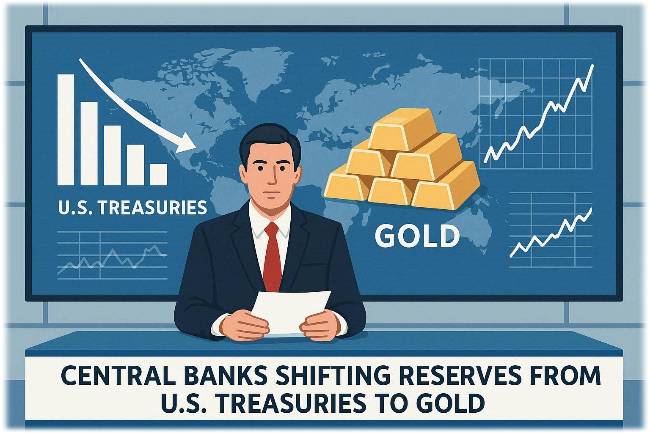

Recent data from the European Central Bank shows that gold now accounts for approximately 27% of global central bank reserve assets.

U.S. Treasuries, by contrast, have declined to roughly 22% of the total. This represents a notable reallocation in the composition of sovereign reserves.

Gold Becomes the Largest Reserve Category

Gold has overtaken U.S. Treasuries as the single largest reserve asset category held by central banks worldwide. This milestone signals a structural shift rather than a temporary fluctuation, reflecting changing priorities among monetary authorities.

Central Bank Gold Purchases Continue

Recent Buying Trends

According to the World Gold Council, central banks remained net buyers of gold in April, adding 17 tons to their reserves. Key purchasers included Poland, China, and the Czech Republic, indicating continued interest across diverse geographic regions.

Consistency of Accumulation

Central bank gold purchases have followed a consistent pattern over recent years. This is not sporadic trading but a sustained accumulation strategy.

Central banks have continued buying gold even during periods when prices have risen significantly, suggesting that these purchases are driven by long-term objectives rather than short-term price considerations.

Why Central Banks Buy Gold

Central banks cite several strategic reasons for accumulating gold:

- Geopolitical risk: Gold is viewed as a hedge against geopolitical instability and uncertainty.

- Sanctions risk: Gold is less vulnerable to foreign policy pressures and financial sanctions compared to assets held in foreign jurisdictions.

- Dollar diversification: Reducing reliance on dollar-denominated assets helps diversify portfolio risk.

These motivations reflect risk management and strategic planning, not speculative trading.

The India Gold Rumor Case Study

The False Rumor

A false rumor circulated claiming that the Reserve Bank of India sold approximately $12 billion in gold to defend the Indian rupee. Both the Reserve Bank of India and India’s official government fact-checking unit denied the claim, clarifying that no such sale occurred.

India’s Actual Gold Holdings

India’s official gold reserves remained unchanged at 880.52 tons during the period in question. Official data confirmed that the central bank did not reduce its gold holdings.

Repatriation Trend

India has been increasing the share of its gold held domestically. Over a six-month period, the proportion of gold stored in India rose from approximately 66% to 77%. This trend suggests a growing preference for holding reserves within national borders.

Why the Rumor Matters

The market’s reaction to the rumor highlights gold’s heightened importance at the sovereign level. Even false reports about central bank gold sales can move markets, underscoring how sensitive investors and policymakers have become to changes in gold holdings.

Structural Shift vs. Short-Term Price Moves

Tactical Volatility Is Normal

Gold prices are subject to short-term fluctuations driven by interest rates, the strength of the U.S. dollar, inflation expectations, and energy-related shocks.

Periods of price weakness are a normal part of gold’s historical price behavior and do not necessarily indicate a breakdown in long-term demand trends.

Analyst Outlook on Gold Prices

Some financial analysts have adjusted near-term price targets for gold due to macroeconomic factors such as inflation, yields, and dollar strength. However, longer-term forecasts remain elevated, reflecting confidence in the underlying structural case for gold.

Separating Price Action from Reserve Behavior

Central bank demand for gold is driven by strategic considerations that operate on a multi-year horizon. Reserve accumulation decisions are not typically based on day-to-day price movements. This means that central banks can continue acquiring gold even when short-term price action is volatile or negative.

Implications for the Global Financial System

Shift Away from Dollar-Centric Reserves

The growing share of gold in global reserves reflects a gradual move away from purely dollar-centric portfolios. While the U.S. dollar remains the dominant reserve currency, central banks are diversifying into assets perceived as more neutral and less exposed to single-country risks.

Gold as a Neutral, Liquid Asset

Gold possesses several characteristics that make it attractive to central banks:

- No counterparty risk: Gold is a physical asset that does not depend on any issuer’s ability to fulfill obligations.

- Global acceptance: Gold is universally recognized and liquid in major financial centers.

- Historical stability: Over long periods, gold has maintained purchasing power and served as a store of value.

These traits make gold appealing for managing sovereign-level risk.

Geopolitical and Sanctions Considerations

Geopolitical tensions and the increased use of financial sanctions have influenced reserve decisions.

Gold is viewed as less vulnerable to foreign policy pressures than assets held in foreign jurisdictions or denominated in foreign currencies. This perception has contributed to the steady accumulation of gold by central banks from diverse regions.

Long-Term Trend, Not a Quick Reversal

Changes in reserve composition occur slowly over years, as central banks adjust portfolios in a deliberate and measured manner. This is a structural trend, not a short-term market swing that can be reversed quickly.

What This Means for Markets and Observers

For Financial Market Participants

Reserve trends can influence long-term sentiment in gold and other safe-haven assets.

Market participants often monitor central bank activity as an indicator of institutional confidence and macroeconomic direction. However, these trends should not be interpreted as signals for short-term trading decisions.

For Policymakers and Economists

Reserve composition affects currency stability, inflation expectations, and international capital flows. Gold’s evolving role is part of broader monetary policy considerations and reflects how central banks manage risks in an increasingly complex global environment.

For General Readers

For readers interested in economics and finance, this development offers insight into how global financial systems evolve over time.

Understanding reserve trends helps contextualize discussions about currency strength, sovereign risk, and the international monetary order.

This article is intended for educational purposes and does not recommend any specific actions.

Common Misunderstandings About Gold and Reserves

Price Changes vs. Volume Changes

A common misconception is that changes in reserve shares always reflect new purchases or sales. In reality, price movements can significantly alter the percentage share of gold in reserves even when holdings remain constant.

Distinguishing between valuation effects and actual volume changes is essential for accurate interpretation.

Speculation vs. Strategic Holding

Another misunderstanding is that central banks treat gold like a speculative asset. In practise, central banks hold gold as a long-term strategic reserve, not as a short-term trade. Their decisions are based on multi-year risk management objectives rather than attempts to profit from price swings.

Media Rumors vs. Official Data

Unverified rumors about central bank gold transactions can spread quickly and influence market perceptions. It is important to rely on official data from central banks, the World Gold Council, and international financial organizations rather than unconfirmed reports.

Conclusion

Key Points Recap

- Gold has overtaken U.S. Treasuries as the largest category in global central bank reserves, accounting for approximately 27% of total reserves.

- Central banks continue to buy gold, with 17 tons added in April alone, led by Poland, China, and the Czech Republic.

- Short-term price volatility does not contradict the long-term structural trend of increasing gold accumulation by sovereign authorities.

Looking Forward

Reserve composition will likely continue to evolve as geopolitical conditions, economic data, and monetary policies change. Readers interested in tracking these developments should monitor official data releases from central banks, the European Central Bank, the World Gold Council, and the International Monetary Fund.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial advice, investment recommendations, or a recommendation to buy, sell, or hold any asset, including gold. All statements reflect publicly available data and general market analysis. Readers should consult a qualified financial professional before making any investment decisions.

MEET THE RESEARCHER

Doug Young Financial Markets Researcher & Former Financial Director

- Over 20 years of experience in financial markets

- More than 15 years specializing in Gold IRAs

- Extensive expertise in precious metals trading

- Former Financial Director at World Freight Services Ltd for 16 years.

- Author of 500+ published financial research articles over 10 years

- Conducted 80+ Gold IRA company evaluations since 2011