TSP Withdrawals

If you are a federal employee with a Thrift savings Plan, at some point you are going to give consideration to a TSP withdrawal. The most common scenarios would be because you change your job and employer, you retire from service, you are still in service and wish to take a loan from your TSP account or you are still in service, reach the age of 59½ and you wish to take advantage of your penalty free entitlement.

All the time you are in federal employment you will not have to pay tax on your TSP contributions but you will have to pay tax on that money when it is withdrawn.

If you decide to make a withdrawal before you become eligible for retirement you could be liable for a 10% IRS tax penalty, But there are exceptions, so let’s start by exploring those:

When Can You Make a TSP Withdrawal With No Penalty?

#1 – Early Thrift Savings Plan Withdrawals

Although federal employees are entitled to make a TSP withdrawal at any time, if you do so before reaching the age of 59½ you will have to pay the 10% IRS penalty in addition to income tax. If however you are still federally employed after getting to that age you are allowed to make a one off withdrawal of just a part or the whole of your funds without incurring a penalty. If you retire at age 59½ you become eligible to make a TSP withdrawal at any time.

If you leave federal employment after reaching the age of 55 but before you get to 59½ you can make a TSP withdrawal without incurring the 10% IRS early withdrawal penalty. If you leave federal employment before you turn 55 however and make a withdrawal before you reach 59½ then the penalty would apply.

You should be mindful of the fact that the funds withdrawn must be declared as income, so choosing to take out a large lump sum could put you in a higher tax bracket. You can avoid that with careful planning. For example you could make a smaller, partial withdrawal.

If you are not a federal employee any more, or you are retired, you have to option to keep the funds in a tax deferred account by rolling them into a Roth IRA or an annuity. If you are still employed, but no longer by the government, you also have the option to rollover the TSP into a traditional IRA, a 401(k), or an annuity.

#2 – Early Retirement

Certain categories of employees are entitled to retire early and make TSP withdrawals without incurring the IRS penalty. For example, federal law enforcement officers, fire fighters and air traffic controllers can retire at any time after they have completed 25 years of service. The retirement age is 50 for any federal employees with 20 years of service. There are additional job types which allow employees to retire at any age once they have completed 25 years of service, subject to agency permission.

Additional ways to avoid the early withdrawal penalty when retiring early are to:

- buy one of Metropolitan Life Insurance’s TSP fixed annuities. This will distribute your funds to you monthly throughout your retirement.

- request life expectancy based monthly payments on IRS Form TSP-70. Payment amounts will be calculated in accordance with the balance in your TSP account, your current age and your life expectancy. Should you stop the monthly payments at any time and request a one off payment of the balance then the 10% IRS penalty will be applied to the lump sum you receive.

#3 – Thrift Savings Plan Loan

Under the terms of the TSP Loan Program you can make a TSP withdrawal by borrowing money from your own account. The amount of loan cannot exceed the total of your contributions and excludes matching contributions.

- A general purpose loan has no restrictions. There is no documentary requirement and repayment must be made in full within one and five years.

- A residential loan allows you to borrow funds from your TSP account to help you purchase or construct your home. This must be your primary home. The repayment terms in this case are anything up to fifteen years.

You have to pay interest on all amounts that you borrow. Payments are automatically deducted from your pay check then these are credited back into your TSP, together with the interest.

#4 – Special Case Penalty Exempt TSP Withdrawals

If you have a disability, either of a physical or mental nature, and it is expected to continue indefinitely, on a permanent basis or become fatal you can take a hardship withdrawal without incurring the 10% IRS penalty. To be eligible a physician will have to confirm your disability.

You can also make a penalty exempt TSP withdrawal:

- to pay any medical expenses which exceed 7.5% of your gross monthly adjusted income.

- to pay higher educational costs for yourself, your spouse, your child or your grandchild.

Thrift Savings Plan Withdrawal Options

Withdrawal Options During Your Employment

TSP Loan Program

Of the two types of available loans (general purpose and residential) you can only have one of each type active at any one time.

You can take out a loan of any amount between $1000 and $50000 provided you have sufficient assets in your account to cover it. The minimum term for each type of loan is one year. For a general purpose loan the maximum term is five years and for a residential loan it’s fifteen years. If you are married your spouse must give their consent to the loan. This applies even if you are separated. The loan processing fee is $50.

Your loan has to be repaid via a deduction from your pay check, but you have the option of making additional repayments from elsewhere. You have to pay interest, which is calculated based on the G Fund rate of return at the time of processing your application. You cannot apply for another loan of the same type until after sixty days of your repayment. Should you leave federal service before repayment is complete you have to repay the balance within ninety days to avoid it being treated as taxable income.

In-Service TSP Withdrawal

The minimum TSP withdrawal you can make is the smallest of either your account balance or $1000. If you are a married FERS employee or uniformed service member your spouse has to give their consent to the withdrawal. If you are a married CSRS employee it is just necessary that your spouse is notified.

The difference between FERS and CSRS employees

Age-based Withdrawals

An ‘aged based’ withdrawal can be requested by any employee over 59½ and this is not subject to any penalties, just income tax. The same employee cannot subsequently request a post employment partial withdrawal however since only one such withdrawal can be made.

Financial Hardship withdrawal

A ‘financial hardship’ withdrawal can be requested by any employee to cover any of these circumstances:

- legal expenses in respect of divorce or separation

- medical expenses, including domestic improvements necessary for medical care

- personal accident expenses

- negative cash flow each month

These types of withdrawals are quite stringent, as the following conditions apply to them:

- Permanent depletion of funds, since they cannot be repaid

- The employee cannot make TSP contributions or receive matching contributions for the subsequent six months (automatic contributions will continue however).

- At the end of this six month period the employee has to make a written application for the contributions to be renewed.

- The withdrawal attracts income tax, plus the early withdrawal penalty if the employee is under 59½.

- This type of withdrawal is limited to one every six months.

Post-Employment TSP Withdrawal Options

While you were in federal service you probably spent years making contributions to the Thrift Savings Plan, building a savings fund for your retirement. Once you have left the service you have to decide what to do with those savings. You can elect for one or a combination of the following alternatives:

Leave Your Funds In The TSP

You could simply leave your funds where they are, as money inside the TSP can continue to be invested and moved around within the Individual Funds .

Bear in mind that you must either withdraw the balance in full or opt for monthly payments by 1st April of the year following the one when you turn age 70½. (Or if you leave federal employment after the age of 70½, the year following the one when you leave). If you don’t comply, the law requires that you are paid an annuity. If you fail to furnish TSP with information for them to purchase the annuity for either you or your spouse your account will be considered abandoned. You could reclaim the abandoned account by choosing a TSP withdrawal option, but in the meantime you would lose the benefit of any earnings on the balance.

Withdraw Some or All of Your TSP Balance

You could opt for one of the following:

Partial withdrawal: A one-off partial withdrawal has to be for a minimum of $1000 and is only an option if you were not in receipt of an age-based withdrawal when you were still in federal service.

A Succession of Monthly Payments: Payments in excess of $25 and made monthly can either be a pre-determined amount or a distribution made in accordance with the IRS ‘life expectancy’ tables. The way it works is that TSP calculators can determine how many payments should be made before your account is exhausted. If these tables are used to make the calculations your monthly payments will change annually taking into account the balance of your account and your age. You have to receive your initial RMD (Required Minimum Distribution) by 1st April of the calendar year following the one in which you reach 70 ½.

A Lump Sum Total Withdrawal: You could make a withdrawal of your TSP in its entirety in one single payment. This could give you tax implications by pushing you into a higher than normal tax bracket for the year in which you make the withdrawal, so you should give this option a lot of thought and give serious consideration to taking independent financial advice if necessary.

Mixed Withdrawal: You could do a mixture of the options outlined, and/or an annuity purchase and/or an IRA rollover.

Unless funds are rolled over or transferred to an IRA all TSP withdrawals are subject to income tax.

Purchase An Annuity

An annuity would provide you with an ongoing flow of income for the rest of your life. It could be an income just for you, or for both you and your spouse (or a different joint annuitant of your nomination).

With a TSP annuity you could choose to be paid either a fixed monthly amount or a different amount which is inflation adjusted from 0 to 3% in accordance with the CPI (Consumer Price Index). The official TSP annuity partner is Metropolitan Life Insurance but you are not restricted to them as you have the option of choosing your own provider.

There are pros and cons with annuities…

The main pro is that your payments are for life irrespective of what age you live to.

The main cons are:

- the risk of inflation – even if you opt for inflation adjusted payments your income would reduce in real terms in times of high inflation.

- reduced inheritance – once the annuity provider receives the money there is nothing left to be inherited. You could get round this by purchasing a cash refund add on or a survivor benefit add on for the annuity, but the cost would come out of your annuity income payments, making them lower each month.

In general terms, annuities are normally considered to be a conservative TSP withdrawal option.

Roll Over or Transfer Your TSP To An IRA

Traditionally the most routine assets held in IRAs are bonds, mutual funds and stocks. Below we are going to introduce you to the exciting option of investing in gold via an IRA, an option which is becoming increasingly popular.

Usually you get more access to your money in an IRA than in a TSP account. You can withdraw funds from an IRA whenever you wish to (subject to income taxes and the IRS early withdrawal penalty of 10% if applicable).

With a Thrift Savings Plan you are restricted to a partial, one-off withdrawal once you have left federal service. Post employment additional withdrawals can only be either your full TSP balance or a succession of payments.

All the time you are in federal service you only have the option to withdraw funds for reasons of financial hardship or, when you are 59½ or older, via a one-off ‘age-based’ TSP withdrawal.

Therefore if you prefer or need access to your funds it could be an advantage to maintain an IRA which is separate to TSP.

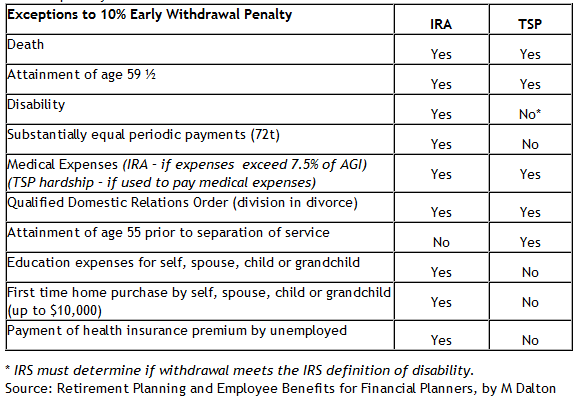

Compared to TSP an IRA offers more options for withdrawals where you can avoid the IRS penalty of 10%.

The following chart, reproduced courtesy of https://fedretire.net, demonstrates this:

Note: Required Minimum Distributions – To comply with IRS requirements minimum distributions must begin by 1st April of the year following the one in which you reach age 70½. This applies to both traditional IRAs and TSP. Failing to do so will result in the imposition of a 50% excise tax on the amount which is not distributed and this % of the distribution increases the older you get.

The distributions are made in accordance with the Uniform Lifetime Table unless the spouse is ten or more years younger than the IRA owner. If that is the case a Joint Life Expectancy Table is applied to determine the distributions.

Differences Between an IRA Rollover and an IRA Transfer

With a transfer the TSP (referred to as your existing IRA custodian) makes out a distribution check and sends it to your new IRA custodian. This can be done for a partial amount or the full amount of your TSP. If partial, this can be done any number of times.

With a rollover your existing IRA custodian (the TSP) sends your retirement funds to you. It is your responsibility to then put this TSP withdrawal into a new IRA. You have to do so within sixty days otherwise the amount withdrawn becomes subject to income taxes. The same funds can be rolled over just once in every twelve month period if you wish to maintain your retirement fund’s tax deferred standing. There is no limit on the amount of partial rollovers you can do however all the time you still have funds in the account.

Benefits of Transferring or Rolling Over your TSP Into a Self Directed IRA

If you have left federal service and you are researching the various options and most beneficial ways to make a TSP withdrawal you should consider transferring or rolling over some or all of your TSP funds into a Self Directed IRA. This allows you to take control of your retirement in a way that a TSP will never do. It will give you much more flexibility and open up limitless investment opportunities for you, including but not limited to gold and other precious metals…

Can You Invest in Gold With a Thrift Savings Plan (TSP)?

Basically the answer is no… however there is a simple solution:

Rollover Your TSP Account To a Gold IRA

There are many good reasons for investing in gold. Many investors nowadays include physical gold in their investment portfolio as a hedge, and so as to protect their overall investment portfolio from the ravages of inflation and economic turmoil.

You can do the same with your retirement fund. This is becoming an increasingly popular practice.

Investing options with TSP accounts are very limited. They only invest in what are referred to as ‘Lifecycle Funds’ (‘L Funds’) and ‘G Funds’. More information about these here: TSP Funds.

This means that in order to invest in gold bullion using the retirement savings that are locked inside your TSP account you need to transfer or rollover your TSP into a special type of Self Directed IRA account commonly referred to as a Gold IRA.

I have a dedicated page with more comprehensive information about converting your Thrift Savings Plan into a Gold IRA here:

TSP Rollover To Gold: Converting Your Thrift Savings Plan To a Gold IRA

BREAKING: Are We Facing a Retirement Crisis?

This video assesses the worrying implications of soaring inflation on your retirement savings:

MEET THE RESEARCHER

Doug Young Financial Markets Researcher & Former Financial Director

- Over 20 years of experience in financial markets

- More than 15 years specializing in Gold IRAs

- Extensive expertise in precious metals trading

- Former Financial Director at World Freight Services Ltd for 16 years.

- Author of 500+ published financial research articles over 10 years

- Conducted 80+ Gold IRA company evaluations since 2011

⚠️ IMPORTANT: All content on this website is for educational purposes only and should not be considered personalized financial advice. Always consult with a qualified financial advisor before making investment decisions.